Modified Adjusted Gross Income (MAGI) is your Gross Income (GI) adjusted for deductions (AGI) and then modified by adding certain deductions back in to calculate MAGI. This page covers MAGI as it applies to Medicaid and the Marketplace. Be aware that the way you calculate MAGI for other tax purposes can differ slightly, so be sure to consult specific IRS instructions for different purposes.

TIP: Use the “find” function on the document (Ctrl+F) to locate specific sections, such as “Worksheet 1-1. Taxpayer’s Modified AGI” in the 8962 instructions. Keep in mind that specifics, such as page numbers, may change each year, so always refer to the latest official forms.

UPDATE 2019: This page provides a general overview. Please note that some details may change yearly, such as line numbers, specific dollar amounts, eligible deductions, and the types of income that need to be added back in. We do our best to keep this information current, but you should always double-check the official documents when calculating your income for tax purposes.

We go pretty in-depth on MAGI and related terms, so here’s a cheat sheet based on information from berkeley.edu (updated for 2019 to reflect recent changes). In most cases, for people receiving tax credits, MAGI will be the same as Adjusted Gross Income (AGI). You can find AGI on your 1040, line 7.

This cheat sheet is designed to simplify the understanding of MAGI for tax credits and cost assistance under the Affordable Care Act.

For tax purposes, follow the instructions on the 8962 worksheet found further down this page. The MAGI cheat sheet is helpful (especially for estimating cost assistance), but following the specific worksheet instructions will ensure you are adjusting your tax credits properly for tax season.

Information for the table above is from berkeley.edu.

MAGI? Modified AGI is your Modified (M) Adjusted (A) Gross Income (GI). You can find a requirement to report “Modified AGI” (MAGI) on Form 8962, Premium Tax Credit (PTC). The form’s instructions include steps for calculating Modified AGI.

Marketplace eligibility is determined based on annual MAGI, while Medicaid and CHIP eligibility are based on current monthly income. In many states, Medicaid/CHIP can also be based on projected MAGI for the remainder of the calendar year. If you are applying for Medicaid, make sure to verify with your state’s Marketplace or Medicaid office. You can review the monthly Federal Poverty Guidelines here for a breakdown of income limits.

Below is a helpful table from healthreformbeyondthebasics.org that explains how Medicaid MAGI has changed in states that expanded Medicaid. For a list of income that is counted as MAGI for Medicaid, refer to the same source (the information is presented below for easy reference, but it’s useful to cross-check both lists).

Both Taxable and non-taxable Social Security income are included in MAGI for determining eligibility for ObamaCare tax credits and Medicaid, but only if the individual has to file taxes.

Social Security Income includes disability payments (SSD and SSDI), pension, retirement benefits, and survivor benefits, but it excludes supplemental security income (SSI). This can be found on Line 20a minus 20b on a Form 1040. Essentially, everything except for SSI counts toward MAGI for ObamaCare and Medicaid eligibility.

ObamaCare calculates the MAGI of the head of household and spouse, while the Adjusted Gross Income (AGI) of tax dependents is also factored in. However, if a tax dependent is not required to file taxes because their income falls below the tax filing threshold, their non-taxable Social Security income is excluded from MAGI. This is because non-taxable Social Security income does not count toward the tax filing limit.

In cases where a tax dependent’s only income is non-taxable Social Security income, they may choose not to file taxes in order to maximize the household’s eligibility for cost assistance. Alternatively, they may opt to file to ensure that the family qualifies for a Marketplace plan with cost assistance instead of Medicaid.

TIP: Survivor benefits can have complex tax rules. Generally, if the benefits are taxable, they count toward MAGI for both the Marketplace and Medicaid. If they are non-taxable, they do not. However, Social Security income specifically is counted toward MAGI for ObamaCare, impacting tax credits and Medicaid eligibility, but only if the individual is required to file taxes.

Social Security Income includes:

• Disability payments (SSD and SSDI)

• Pension

• Retirement benefits

• Survivor benefits

It excludes Supplemental Security Income (SSI). You can find this reflected on Line 20a minus 20b of a Form 1040.

In general, all Social Security income except for SSI counts toward MAGI for ObamaCare and Medicaid. However, in the case of a child, if they don’t have sufficient taxable income, it may not count (refer to the IRS rules for children here).

For help in determining what you qualify for, you can contact the Marketplace or your local Social Security Office for assistance.

What is SSI? SSI stands for Supplemental Security Income, a government program that provides stipends to low-income individuals who are aged (65 or older), blind, or disabled. It is administered by the Social Security Administration but funded by the U.S. Treasury’s general funds, not the Social Security Trust Fund. Therefore, SSI does not count for ObamaCare or Medicaid eligibility or cost assistance.

Health Savings Accounts (HSA’s), retirement accounts like 401(k)s, and other tax-advantaged investment vehicles can be a great way to lower your Gross Income (GI), Adjusted Gross Income (AGI), and Modified Adjusted Gross Income (MAGI). Specifically for ObamaCare, HSA’s really stand out.

Not only can an HSA lower your MAGI (since it lowers your AGI and isn’t added back to MAGI), but it also allows you to accumulate interest tax-free and spend money on out-of-pocket medical, dental, and vision expenses tax-free. These healthcare savings can really add up!

However, you need to have a high-deductible health plan to qualify for an HSA, and it’s important to be mindful of your income. Overfunding an HSA can put you under subsidy floors if your income is low, but strategic funding can help you stay under subsidy ceilings (like 400% of the Federal Poverty Level) if your income is high. See our page on HSAs and our page on retirement accounts to learn how to lower your MAGI for ObamaCare tax credits and cost-sharing reduction subsidies.

NOTE: Not all deductions that lower GI will lower MAGI. Some tax-advantaged vehicles have specific requirements and risks. Review what is added back into MAGI, and consider seeking professional tax advice.

Below is a breakdown of income types that are commonly counted for health insurance tax credits. The list is from HealthCare.Gov and is based on the full list from the IRS. This will help you determine what income is factored into your eligibility for tax credits under the Affordable Care Act (ObamaCare).

| Income type | Included? | Notes |

|---|---|---|

| Federal Taxable Wages (from your job) | Yes | If your pay stub lists “federal taxable wages,” use that. If not, use “gross income” and subtract the amounts your employer takes out of your pay for child care, health insurance, and retirement plans. |

| Tips | Yes | |

| Self-employment income | Yes | Include “net self-employment income” you expect — what you’ll make from your business minus business expenses. Note:You’ll be asked to describe the type of work you do. If you have farming or fishing income, enter it as either “farming or fishing” income or “self-employment,” but not both. |

| Unemployment compensation | Yes | |

| Social Security | Yes | Include both taxable and non-taxable Social Security income. Enter the full amount before any deductions. |

| Social Security Disability Income (SSDI) | Yes | But do not include Supplemental Security Income (SSI). |

| Retirement or pension Income | Yes | Include most IRA and 401k withdrawals. (See details on retirement income in the instructions for IRS publication 1040). Note:Don’t include qualified distributions from a designated Roth account as income. |

| Alimony | Yes | |

| Child support | No | |

| Capital gains | Yes | |

| Investment income | Yes | Include expected interest and dividends earned on investments, including tax-exempt interest. |

| Rental and royalty income | Yes | Use net rental and royalty income. |

| Excluded (untaxed) foreign income | Yes | |

| Gifts | No | |

| Supplemental Security Income (SSI) | No | But do include Social Security Disability Income (SSDI). |

| Veterans’ disability payments | No | |

| Worker’s Compensation | No | |

| Proceeds from loans (like student loans, home equity loans, or bank loans) | No |

All of the terms below are directly related to understanding how MAGI applies to the Affordable Care Act and cost assistance. Terms are defined further in the 8962 instructions.

Household income (Family income) = Household or family income for the ACA is MAGI of the head of household (and spouse if filing jointly) plus the AGI of anyone claimed as a dependent.

Federal Poverty = The ‘Federal Poverty Guidelines‘ show what percentage of the ‘Federal Poverty Level’ a family’s household income puts them at. They differ for Hawaii and Alaska. For the ACA, the amount is based on MAGI, but MAGI is calculated slightly differently when applying it to Medicaid versus the Marketplace (see chart below for clarification).

Premium Tax Credits = Premium tax credits are cost assistance for health insurance premiums. They can be taken in advance on any Marketplace plan and then claimed or adjusted using form 8962 at the end of the year.

Gross Income = Total income before deductions.

Adjusted Gross Income (AGI) = Income adjusted for deductions.

Modified Adjusted Gross Income (MAGI) = Income adjusted for deductions, with certain income added back in (see full list below).

Modified adjusted gross income (MAGI) can be calculated by following the IRS instructions, and the steps outlined here are based on the official IRS 8962 instructions. While the simplified methods on this page are useful, for tax purposes, it’s important to follow the official methodology line-by-line.

If you’re calculating MAGI for the Premium Tax Credit using Form 8962), the steps below will guide you through the process. For other tax forms, such as Form 8582 (related to passive activity losses), you can use the IRS MAGI calculator.

NOTE: While this page offers guidance for understanding the steps, it is essential to consult the official IRS instructions or seek the help of a tax professional for accurate tax reporting.

Enter your modified AGI on line 2a. Use the worksheet below to figure your modified AGI from your tax return.

| 1. | Enter your adjusted gross income (AGI)* from Form 1040, line 7, or Form 1040NR, line 36 | 1. | |

| 2. | Enter any tax-exempt interest from Form 1040, line 2a, or Form 1040NR, line 9b | 2. | |

| 3. | Enter any amounts from Form 2555, lines 45 and 50, and Form 2555-EZ, line 18 | 3. | |

| 4. | Form 1040 filers: If line 5a is more than line 5b, subtract line 5b from line 5a and enter the result | 4. | |

| 5. | Add lines 1 through 4. Enter here and on Form 8962, line 2a | 5. | |

| *If you are filing Form 8814 and the amount on Form 8814, line 4, is more than $1,050, you must enter certain amounts from that form on Worksheet 1-2. See Form 8814 under Line 2b below. | |||

If the amount on line 6 of Worksheet 1-1 above is less than zero, seeLine 3, later, before you enter an amount on Form 8962, line 3.

Enter the modified AGI for all of your dependents on line 2b. Use the worksheet below to figure the combined modified AGI for the dependents claimed as exemptions on your return. Only include the modified AGI of those dependents who are required to file a return. Do not include the modified AGI of dependents who are filing a tax return only to claim a refund of tax withheld or estimated tax.

| 1. | Enter the AGI* for your dependents from Form 1040, line 7, and Form 1040NR, line 36 | 1. | |

| 2. | Enter any tax-exempt interest for your dependents from Form 1040, line 2a, and Form1040NR, line 9b | 2. | |

| 3. | Enter any amounts for your dependents from Form 2555, lines 45 and 50, and Form 2555-EZ, line 18 | 3. | |

| 4. | For each dependent filing Form 1040: If line 5a is more than line 5b, subtract line 5b from line 5a and enter the result | 4. | |

| 5. | Add lines 1 through 4. Enter here and on Form 8962, line 2b | 5. | |

| *Only include your dependents who are required to file an income tax return because their income meets the income tax return filing threshold. | |||

If the amount on line 6 of Worksheet 1-2 above is less than zero, see Line 3, later, before you enter an amount on Form 8962, line 3.

Family Income or Household Income is commonly referred to when discussing the Affordable Care Act (ACA). This is typically your Modified Adjusted Gross Income (MAGI), plus the Adjusted Gross Income (AGI) of any dependents in your household who are required to file tax returns.

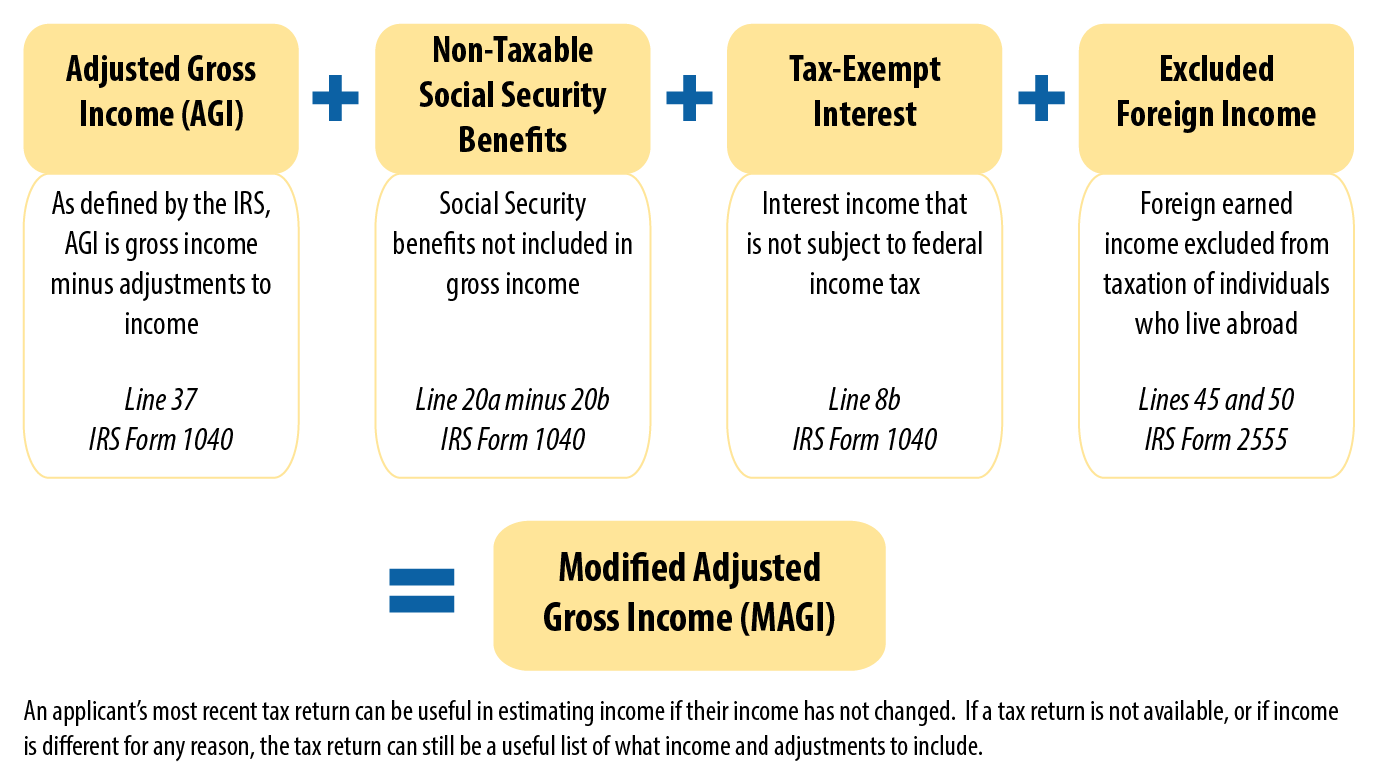

Modified AGI (MAGI) includes Adjusted Gross Income on your federal income tax return plus any excluded foreign income, nontaxable Social Security benefits (including tier 1 railroad retirement benefits), Supplemental Security Income (SSI), and tax-exempt interest received or accrued during the taxable year.

You won’t find MAGI on your 1040, but you will find Modified AGI on Form 8962, Premium Tax Credit (PTC), the form you use for reporting Marketplace cost assistance. If you are looking at past tax returns, look at Adjusted Gross Income (AGI) and take it from there. In most cases, it’s a similar amount.

MAGI, in most cases is simply your Adjusted Gross Income plus taxable interest found on lines 37 and 8b of your IRS from 1040. Take a look at the form. You’ll see big sections on Income and Adjusted Gross Income. If you don’t think your income will change, you can base everything on that information. See the full How to Calculate Modified Adjusted Gross Income (MAGI) video.

We cover MAGI on our subsidy calculator page, but since it’s so important to the ACA, we will do a detailed breakdown of MAGI and the other income types below.

FACT: When you apply for coverage through the Marketplace, all the necessary calculations for determining your cost assistance (such as premium tax credits and other subsidies) will be automatically handled for you. However, understanding how this process works ensures you are receiving the correct amount of assistance. This knowledge is especially helpful if you file your taxes manually.

By learning how to utilize available tax deductions, you can potentially reduce your taxable income, saving money during tax season and lowering the cost of your health insurance premiums.

For the Affordable Care Act (ACA), MAGI is used for:

Determining Marketplace Cost Assistance: MAGI helps calculate how much cost assistance (such as tax credits and cost-sharing subsidies) you are eligible for. You’ll use your projected MAGI for the upcoming year to determine your assistance level. Later, you’ll adjust that amount on your year-end taxes. Misunderstanding MAGI can result in owing money or missing out on subsidies. Be sure to update the marketplace with any life changes to avoid receiving incorrect assistance.

Determining Medicaid or CHIP Eligibility: MAGI is also used to assess whether you qualify for Medicaid or CHIP. Eligibility can be based on past or future MAGI, along with other factors like household size, income, age, and disability, especially in states that did not expand Medicaid.

Calculating Your Federal Poverty Level (FPL) Percentage: Once you know your MAGI, it’s easy to determine where you fall on the Federal Poverty Level scale. The FPL is used to decide eligibility for both cost assistance and Medicaid/CHIP. It’s also important for many other assistance programs that you may qualify for. See our Federal Poverty Guideline page for details on all of this.

Figuring Out if You Owe the Shared Responsibility Payment: If your gross income is below the filing threshold, you won’t need to pay the Shared Responsibility Payment. However, some assistance programs still rely on MAGI, so understanding it is useful even if you’re not required to file.

The information provided here is compiled from reliable sources such as HealthCare.Gov, Zane Benefits, IRS, and TurboTax.

Modified Adjusted Gross Income (MAGI) is a measure used by the IRS to determine eligibility for certain deductions, credits, or retirement plans. For health insurance purposes, MAGI plays a crucial role in determining your eligibility for premium tax credits and cost assistance subsidies under the ACA. The IRS phases out tax credits as income increases, and MAGI is used to figure out your total earnings by adding certain income factors back to your Adjusted Gross Income (AGI). Starting in 2014, MAGI has been essential for determining eligibility for subsidies and tax credits on the Health Insurance Marketplaces.

Adjusted Gross Income (AGI) is the total income of your household after certain adjustments. AGI is calculated before applying itemized or standard deductions, exemptions, or credits, making it the baseline for further tax calculations.

AGI is found on:

Your Modified Adjusted Gross Income (MAGI) is the sum of your household’s Adjusted Gross Income (AGI) plus certain types of income that were excluded from AGI. MAGI is used to determine eligibility for various tax credits and deductions, including health insurance cost assistance under the ACA.

• Adjusted Gross Income (AGI, as defined by IRS)

• Plus: Excluded foreign income

• Plus: Tax-exempt interest

• Plus: Non-taxable Social Security benefits

• Equals: MAGI

Income Counted Toward MAGI:

MAGI includes all the income types counted in AGI, as well as any tax-exempt interest and other additions like excluded foreign income and non-taxable Social Security benefits. It’s important to understand which types of income are included in MAGI to calculate health insurance subsidies and Health Savings Account (HSA) contributions accurately. Be sure to check official IRS documents for the latest amounts and specific rules regarding what counts toward MAGI.

Income Counted Under MAGI:

Earned Income

Wages, salaries, tips

Self-employment, business and farm income after deduction of business expenses (including depreciation and capital losses)

Unearned Income

Interest (taxable and non-taxable)

Social Security (SSA) income

Dividends

Taxable state income tax refunds and credits

Portion of scholarships, awards or fellowship grants used for living expenses

Alimony received

Capital/other gains

IRA distributions (taxable amount only)

Pensions and annuities

Rental real estate income and royalties

Unemployment Compensation

Other income if taxable (such as prizes, jury duty pay not given to employer, etc.)

MAGI Income Deductions:

Business/Self-employment expenses, include:

farm expenses,

depreciation,

capital losses (limited to $3,000 in a tax year or $1,500 if married and filing separately),

rental/real estate losses,

partnership and S Corporations losses, and

royalties loss

Estate and trust loss

Educator expenses (limited to $250 per educator in a tax year)

Real estate mortgage investment loss

Business expenses of Reservists, Performing Artists, and Fee-Basis Government Officials

Health Savings Account Deduction (limited to $271/month for single filer, and $538/month for a family)

Moving Expenses (if you moved in connection with new job)

Tax deductible part of self-employment tax

Self-employed SEP, SIMPLE, and qualified plans

Self-employed health insurance deduction

Penalty on early withdrawal of savings

Alimony paid

IRA deduction

Student loan interest (limited to $2,500 in a tax year)

Tuition and fees (limited to $4,000 in a tax year)

Domestic production activities deduction (up to 9% of qualified production activities)

NOTE: For MAGI, alimony paid must be entered under the Miscellaneous Expense screen in the IES Worker Portal (for non-MAGI, you enter alimony paid on Support Expenses screen). IES does not track annual caps for MAGI income deductions. Workers must ensure that deductions that exceed the annual caps are not entered. For example, if a teacher reports $50 per month in educator expenses from January through June, the cap of $250 will have been reached by May. Do not allow the expense for the remaining months of the calendar year.

Income Deductions Not Considered Under MAGI:

The following income deductions will no longer apply to MAGI groups:

$90 employment deduction for employed persons

the $30 plus 1/3 earned income exemption (EIE)

child care expenses

child support that was paid to someone not in the household

Income Not Counted Under MAGI

Child support income received

Worker’s Compensation

Veteran’s Benefits

Supplemental Security Income (SSI)

Portion of scholarships, awards or fellowship grants used for qualifying education expenses

Native American and Alaska Native (AI/AN) income derived from distributions, payments, ownership interests, real property usage rights, and student financial assistance provided under the Bureau of Indian Affairs education programs.

This list of what is considered MAGI is from a TurboTax article on HSAs. Learn more about MAGI here or read the IRS’ explanation of MAGI.

Your gross income refers to the total money earned from various sources, including wages, interest, dividends, rental and royalty income, capital gains, business income, farm income, unemployment, and alimony. This serves as the foundation for calculating your Adjusted Gross Income (AGI).

Gross income encompasses salary, interest earned, income from investments, and any revenue generated through business, trade, or investments.

After determining your gross income, you “adjust” it to calculate your Adjusted Gross Income (AGI). This is done by subtracting qualified deductions from your gross income.

These adjustments may include contributions to IRAs, moving expenses, alimony paid, self-employment taxes, and student loan interest.

Many free AGI calculators are available online to assist with these calculations.

To calculate your Modified Adjusted Gross Income (MAGI), you start with your Adjusted Gross Income (AGI) and then “modify” it by adding back specific deductions. These include:

• Deductions for IRA contributions.

• Deductions for student loan interest or tuition.

• Excluded foreign income.

• Interest from EE savings bonds used to pay for higher education expenses.

• Employer-paid adoption expenses.

For most people, MAGI is the same as AGI, but certain deductions may cause these numbers to differ.

![]()

ObamaCare: Modified Adjusted Gross Income (MAGI)

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a.

ObamaCareFacts is a free informational site. It's privately owned, and is not owned, operated, or endorsed by the US federal government or state governments. Our contributors have over a decade of experience writing about health insurance. However, we do not offer professional official legal, tax, or medical advice. See: Legal Information and Cookie Policy. For more on our company, learn About ObamaCareFacts.com or Contact us.